If there’s one country where Revolut is an indispensable part of the payments landscape, it’s the Republic of Ireland. But Revolut’s Irish success comes at the expense of uncertainty regarding the protection of client funds.

Revolut is a hit in Ireland

“In Ireland people say, ‘We’ll Revolut that to you’ because it’s the quickest and cheapest way to move money,” an Irish payments expert told me last week.

Faster payments schemes, usually operated by central banks, more or less eliminate settlement risk: the whole payments process, from the transmission of the payment message to the arrival of funds in the payee’s account, occurs in real time and 24/7.

“It’s the quickest and cheapest way to move money”

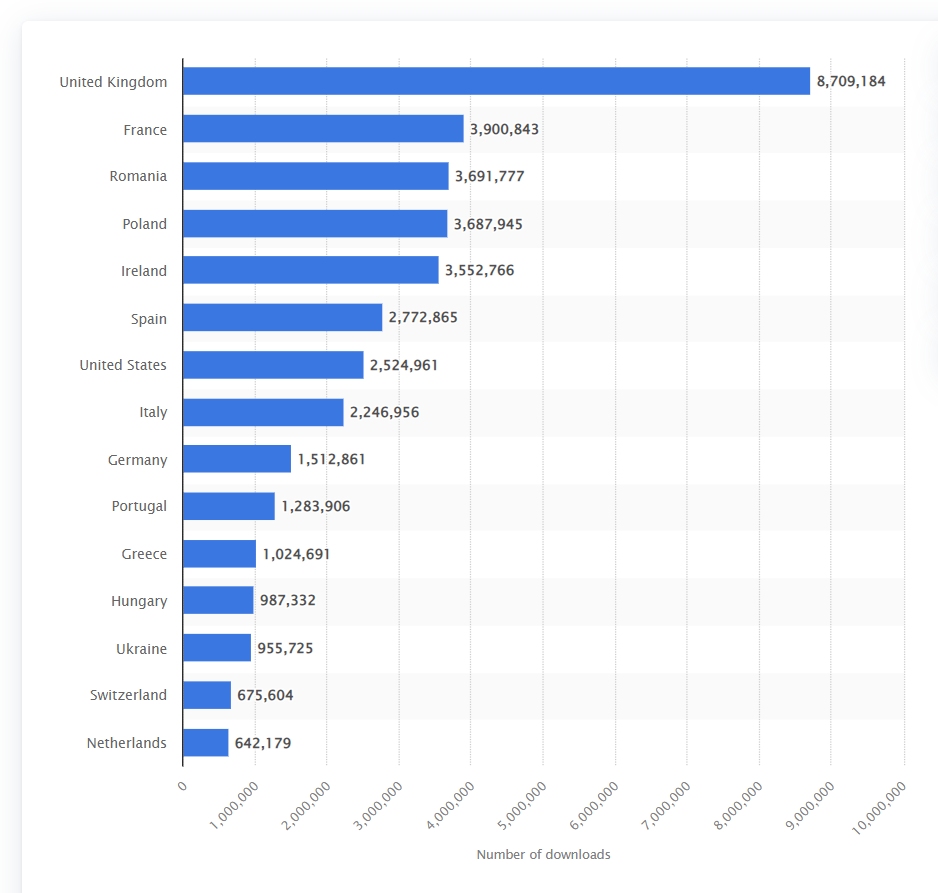

At the latest count, 55 countries have faster payments schemes. But Ireland doesn’t and Revolut is filling the gap: the country has seen over 3.5 million downloads of the financial technology (fintech) firm’s app, according to Statista.

Revolut downloads by country (Feb 2023, Statista)

When compared to Ireland’s 5 million population, this represents the highest penetration rate for Revolut in any single country. Revolut has more than doubled its Irish client base in less than a year.

It also now claims over 25 million retail users worldwide, up from 1.5 million in 2018, as well as over 500,000 business users.

Legal manoeuvring

But the payment app’s rise to prominence in Ireland has involved some complex legal manoeuvring, with implications for the way Irish clients’ money is protected.

Initially, Revolut operated in Ireland under a ‘passported’ UK e-money licence, obtained in 2018 from the Financial Conduct Authority.

This left Revolut’s Irish clients—like its UK ones—reliant on the ‘safeguarding’ procedures for client money at UK electronic money institutions (EMIs).

As EMIs are not banks, they do not offer deposit insurance. Safeguarding is an approach whereby customer funds are supposed to be kept separate from the financial product provider’s own money at all times.

Brexit meant that, from the end of 2020, Revolut’s UK’s e-money licence could no longer be passported to Ireland. So during that year the firm said it was migrating its Irish customers to a Lithuanian entity with a Lithuanian e-money licence.

This move would be temporary, though, Revolut said.

“Our plan is that once the business in Ireland is authorised by the Central Bank of Ireland, we will migrate our Irish Revolut customers to the Irish entity and, in due course, many of our other western European customers,” the firm said in October 2020.

Revolut got an Irish e-money licence in December 2021, having waited a year and a half. But in the same month Revolut extended and supplemented a banking licence it had earlier obtained in Lithuania.

And in February 2022 the fintech said it was going to migrate its Irish clients again, this time to Revolut Bank UAB, that Lithuanian banking entity.

As a result of these legal changes, anyone with a Revolut account in Ireland is now a client of the Irish branch of a Lithuanian bank.

The same applies to Revolut clients in Belgium, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Lichtenstein, Luxembourg, Netherlands, Poland, Romania, Spain and Sweden.

UK-based Revolut users remain clients of the local e-money institution, Revolut Limited.

Revolut users in the US have a relationship with Revolut Technologies Inc., a technology services provider. This firm is the administrator of a Visa card program issued by a separate entity, Metropolitan Commercial Bank.

On Monday this week, Metropolitan Commercial Bank’s share price fell by 44 percent amidst a rout in US regional bank shares following Friday’s insolvency of Silicon Valley bank. Metropolitan Commercial’s share price recovered on Tuesday but is still down 41 percent this year.

If you’re unsure which Revolut entity you’re dealing with, check the small print at the bottom of the Revolut website in your own country.

What happens in the case of bank insolvency?

If Revolut’s Lithuanian bank (Revolut Bank UAB) were to become insolvent, the fintech’s Irish clients would have to turn to the Lithuanian state deposit insurance fund to get back any money they had on their cards.

According to the firm, the Lithuanian insurance fund promises to guarantee individual deposits of up to €100,000 and to pay compensation for deposits at a failed bank within ten working days.

But is this promise reliable? According to Hungary’s central bank, it’s not.

On Monday the Hungarian National Bank (HNB) published a press release urging Revolut to set up a subsidiary in Hungary, where it would be subject to local regulations and capital requirements, rather than passporting its services into the country from the Lithuanian bank. The HNB made a similar request last year.

The HNB referred to Revolut’s recently qualified accounts, saying:

“According to British and domestic press reports published in recent days, Revolut Ltd.’s auditor indicated that there is a risk that the British company’s 2021 income statement contains material errors. The lack of auditor approval of the data in the company’s books is considered a significant risk element for any economic company, but especially for a multinational financial institution.”

Hungary’s central bank also said that Revolut had put Hungarian clients in a disadvantageous position.

“Should a Hungarian customer incur any settlement, consumer or deposit insurance problem, he may essentially seek legal remedy in connection with the dispute only in Lithuania (subject to international arbitration procedure), presumably in Lithuanian or English,” the HNB said.

The central bank said that Hungarian customers would be better off if they could fall back in an emergency on their own country’s deposit insurance scheme—something that would happen automatically if Revolut set up a local banking subsidiary.

Hungary’s central bank says it’s not against new fintech innovations that enable simpler, cheaper financial services, “but only if they guarantee financial stability and customer safety”.

the fund does not have agreed credit lines in place

Lithuania’s insurance fund—operating out of a country with a 2.8 million population—also underwrites the deposits of Revolut Bank UAB’s customers in Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Lichtenstein, Luxembourg, Netherlands, Poland, Romania, Spain and Sweden—where aggregate downloads of the app have now exceeded 20 million.

According to the European Banking Authority, the Lithuanian fund held €153m at the end of 2021, 0.8 percent of the total insured deposits covered by the scheme. The deposit insurance fund is funded by a levy on local banks, including Revolut.

As at March 2023, the fund’s size had grown to €287m. However, the EBA said, the fund does not have agreed credit lines in place and would need to borrow from other countries’ deposit guarantee schemes, the Lithuanian government or commercial banks if it got into trouble.

Home/host supervision

In 2008, the failure of Icelandic bank Landsbanki, showed the inherent weakness of a reliance on supervision in a single home country for a financial institution operating cross-border.

Landsbanki had marketed high-interest online savings accounts under the name ‘Icesave’ in the UK and the Netherlands, using a branch network to do so, rather than separately capitalised subsidiaries.

The bank’s collapse forced governments in both the UK and the Netherlands to intervene and guarantee their citizens’ lost deposits in full.

In 2014, the Bank of England outlined a new supervisory regime, under which foreign banks operating in the UK market would generally have to operate as subsidiaries, putting them on the same footing as banks that are run from Britain. It’s this approach that’s now being called for by Hungary’s central bank for Revolut.

During the recent collapse of Silicon Valley bank, the existence of the bank’s UK operations as a separate subsidiary enabled British authorities to organise a rapid sale of SVB UK separate from the insolvency proceedings taking place in the US.

After a week in which three US banks failed, there are likely to be many new questions about the safety of client money.

Revolut’s spectacular success in Ireland shows how quickly new payments technology can take root. But the complex cross-border exposures involved in the company’s expansion show that these questions are hard to answer with any certainty.

*Article updated after publication to include Hungarian central bank’s comment about Revolut’s qualified accounts

Sign up here for the New Money Review newsletter

Click here for a full list of episodes of the New Money Review podcast: the future of money in 30 minutes

Related content from New Money Review

Revolut blocked large Friday withdrawal, says VC firm

No clarity on Revolut safeguarding

Silicon Valley bank run depegs USDC