Terra, the third-largest stablecoin by market size, is trading at a discount to its dollar peg after heavy investor selling that threatens broader contagion effects.

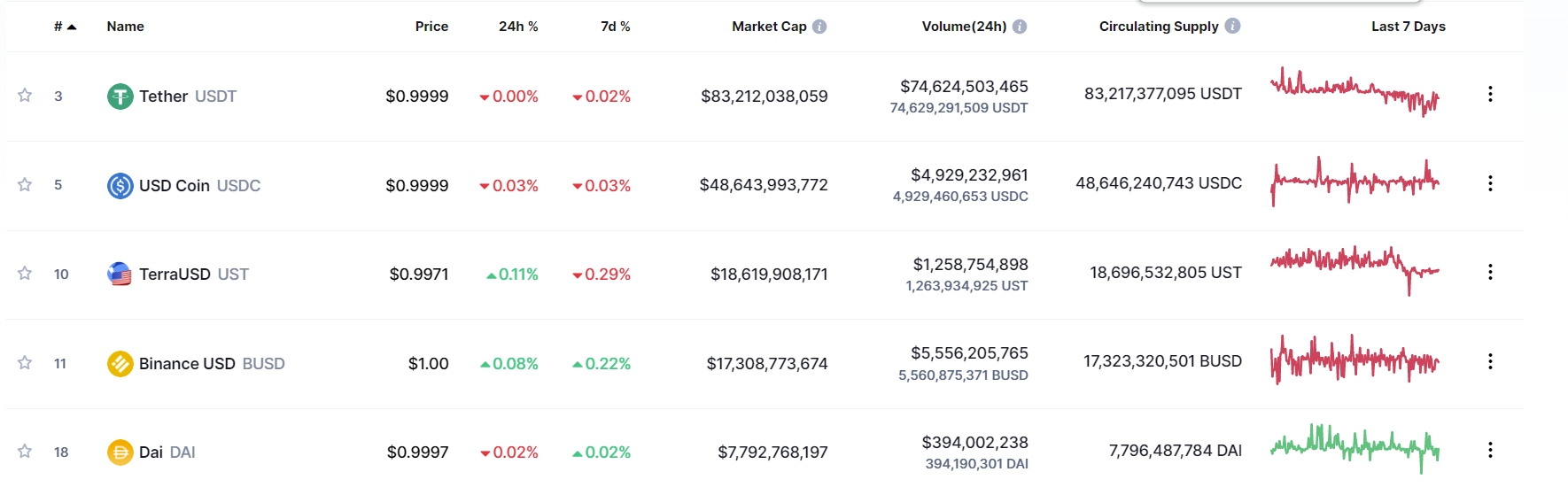

With a market capitalisation of over $18bn, Terra (UST) has risen to prominence in the last year. Its market capitalisation was just $2.9bn in September 2021.

Top five stablecoins by market size (May 2022)

But by comparison with most other stablecoins, which claim to hold reserves of dollar-denominated assets to back their one-to-one dollar peg, Terra uses a more controversial mechanism to stabilise its market value.

Terra’s dollar peg depends a related cryptocurrency token called Luna, whose value floats freely: at any time, market participants can exchange a single Terra token for a dollar’s worth of Luna (and vice versa).

“Terra is effectively collateralised by the governance token Luna,” Bennett Tomlin, co-host of the Crypto Critics podcast, said last week.

“As long as Luna is valuable and as long as enough people think the currency-like thing is valuable, then it continues working. The issue becomes if people stop believing either of those things.”

In the last week, however, Terra has traded below its peg, while the value of Luna has fallen by about a third, casting doubt on the stabilisation mechanism.

Terra loses peg

Luna loses a third of its value in a week

Another source of instability for Terra is the depletion of the deposits in a borrowing and lending protocol that has acted as a substantial source of demand for the stablecoin during the last year.

Deposits in the Anchor protocol, which is run by Terraform Labs, the creator of Terra and Luna, have fallen by around $3bn over the weekend.

Anchor has attracted interest from participants in the decentralised finance (DeFi) market by promising dollar interest rates of 20 percent.

“By paying out this interest rate, they hope to help drive demand for Terra and they hope it continues to grow to such a point that it hits some kind of inflection point where there’s such exogenous demand for it that you no longer need to do the unsustainable things,” said Crypto Critics podcast’s Tomlin.

The founders of Terraform Labs and the venture capitalists that backed Terra have large financial interest in keeping things growing, said Tomlin.

According to Tomlin and his co-host Cas Piancey, 56 percent of the original offering of Terraform Labs’ Luna token was distributed amongst founders and venture capitalists at prices of either $0.18 or $0.80.

With the Luna price peaking in April this year at nearly $120 a token, these early investors made up to 666 times their initial investment.

“It doesn’t matter if it eventually fails because we’ve told everyone this was an experiment”

Tomlin said that the founders of such cryptocurrency projects are all too ready to walk away when things go wrong. He cited the recent boom in DeFi as having created extra risks.

“There’s a reason [algorithmic stablecoins] pop up every time there’s a big DeFi surge, because they depend on this alchemy of essentially creating something from nothing,” said Tomlin.

“It is very easy to play games with them, right? Set up a lending game that could run for long enough that a lot of people make money from it. And it doesn’t matter if it eventually fails because we’ve told everyone this was an experiment.”

In March, Terra said it would add up to $10bn in bitcoin to its reserves, aiming to provide an additional source of stability to the stablecoin.

However, critics believe the stablecoin will still eventually fail.

“Terra’s mechanism for pegging UST to USD has stress-amplifying properties that allow even not so large contractions to trigger a death spiral,” Hjalmar Peters, a cryptocurrency trader, wrote on April 30.

“In order to prevent these weaknesses from surfacing, Terra incentivises UST supply expansion. It does so by offering an artificial 19.5 percent interest rate on UST and relying on Ponzi’s method for converting principals and interests back to USD. This approach is obviously not sustainable.”

“When the outflow of principals and interests eventually exceeds the inflow of newly attracted money, then the induced expansion will turn into an all the more pronounced contraction,” said Peters.

An open question is how any failure of Terra might spread contagion to the broader cryptocurrency market.

A popular Youtube video on how to deposit Terra tokens at Anchor to earn 20 percent interest showed that holders of US dollars had to pass at least six intermediaries to do so: a bank account, the US Automated Clearing House (ACH) payments network, cryptocurrency exchange FTX, dollar stablecoin Tether, crypto exchange Kucoin, the cryptocurrency network Tron and then Terra.

Deposits of Terra tokens have also been used to underpin even riskier cryptocurrency ventures.

In January, a DeFi protocol called Abracadabra failed after one of its founders was revealed to have been a co-founder of the fraudulent Canadian cryptocurrency exchange Quadriga.

Abracadabra had rehypothecated the Terra tokens deposited on Anchor to increase the interest rate earned to over 100 percent.

Sign up here for the New Money Review newsletter

Click here for a full list of episodes of the New Money Review podcast: the future of money in 30 minutes

Related content from New Money Review