Is tether a fraud or a threat to the hegemony of the US dollar?

Nothing better illustrates the clash between traditional finance and the new world of cryptocurrencies than tether, a digital token invented in 2014.

By contrast with cryptocurrencies like bitcoin, whose fiat currency value has fluctuated wildly (and generally risen) since its inception, a so-called stablecoin like tether has a more mundane objective: maintaining parity with one of the world’s established currencies.

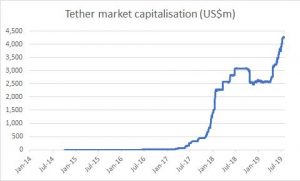

Tether, despite a few wobbles, has managed to hang on to its one US dollar target value since its launch.

Source: Coinmetrics

But tether’s key selling point gives little hint of the controversies it has ignited.

For its detractors, tether is a ponzi scheme that is used to prop up the price of bitcoin.

“The primary utility of crypto is money laundering”

It has other nefarious uses, say critics.

“The primary utility of crypto is money laundering. That is why the US Treasury will crush it,” Christopher Whalen, an author and the founder of Institutional Risk Analyst, tweeted on August 5.

In fact, the creators of tether are already in deep water with US law enforcement agencies.

Tether (the legal entity that issues tether tokens) faces allegations of fraud in the New York state courts, where the Attorney General has provided evidence that the cryptocurrency is less than fully backed by dollar reserves. The New York prosecutor’s lawsuit also names the Bitfinex cryptocurrency exchange as a respondent.

“Our investigation has determined that the operators of the Bitfinex trading platform, who also control the tether virtual currency, have engaged in a cover-up to hide the apparent loss of $850m of commingled client and corporate funds,” Letitia James, the New York Attorney General, said in April.

But the users of the cryptocurrency so far appear oblivious to such claims. This year, tether’s market capitalisation has grown to over $4bn and the digital substitute for the US dollar is reportedly seeing new applications.

Source: Coinmetrics

According to Coindesk, Chinese merchants selling goods in Russia are now using tether as the most efficient way of repatriating their local rouble earnings.

Transfers using tether sidestep both the US banking system and the Chinese central bank’s capital controls

When in Moscow, these merchants spend up to $30m a day buying tether from currency dealers, says Coindesk, then repatriate the cryptocurrency tokens to China, where they can easily sell them.

Tether enables the merchants to exchange Russia’s currency, which has limited international convertibility, into something that’s tradeable across borders.

Transfers using tether also sidestep both the US banking system (where all movements of dollars are tracked) and the Chinese central bank’s capital controls, which limit the amount of foreign currency anyone can buy or sell to $50,000 a year.

The outcome of the lawsuit surrounding Bitfinex and Tether remains uncertain. A New York Supreme Court judge recently deferred a decision on whether to compel Tether to turn over documents.

But in the longer term the tether saga could have broader, geopolitical implications.

US regulators may still succeed in bringing tether’s operators to heel and in cracking down on what they see as an unlicensed money transfer business.

But what if the cryptocurrency’s use—or that of tokens modelled on tether—confounded critics and expanded much further, creating an offshore dollar market that’s out of the control of the US government?

An unregulated cryptocurrency token that facilitated dollar payments more seamlessly and cheaply than US banks could undermine the US financial system altogether.

Where tether came from

Tether was invented to help cryptocurrency traders and exchanges get around the many roadblocks separating the emerging crypto infrastructure from the traditional financial system.

To this day, many companies involved in cryptocurrency face great difficulty obtaining a bank account, with banks wary of getting involved with activities for which they might later face sanction from regulators.

“Regulators couldn’t get their heads around cryptocurrency”

“I came up with the idea for tether in late 2013,” Phil Potter, the former Chief Strategy Officer of Bitfinex, said on the What Bitcoin Did podcast in May this year.

“At the time there was no regulation of cryptocurrency exchanges. Regulators couldn’t get their heads around cryptocurrency.”

Potter and Giancarlo Devasini, Bitfinex’s CFO, were instrumental in setting up Tether, teaming up in 2014 with Brock Pierce, Reeve Collins, and Craig Sellars, who had set up a precursor to tether called Realcoin.

Potter’s proposed solution to the lack of banking access for crypto exchanges was to create distinct legal entities for crypto trading and for dealing with banks, and to use tether, rather than real dollars, euros or yen, as the future settlement asset for all crypto activity.

“It seemed at the time that running a crypto-only exchange was easier. If we could separate the crypto operations from the fiat operations there seemed a greater chance we could achieve regulatory certainty,” Potter said.

“All the top crypto exchanges use tether. Why? Because banking is almost impossible”

Although at the outset, by Potter’s own admission, Bitfinex struggled to get other exchanges to use tether, this changed when traders started to use tether to arbitrage discrepancies in the pricing of bitcoin and other cryptocurrencies across different global exchanges, starting in 2015.

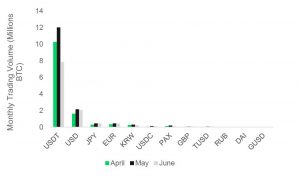

Now, cryptocurrency trading activity denominated in tether outweighs trading in traditional currencies.

In June 2019, for example, trades in bitcoin against tether (ticker symbol USDT) represented around 70 percent of all global exchange-based activity in bitcoin, according to data provider CryptoCompare.

“All the top crypto exchanges use tether. Why? Because banking is almost impossible,” Potter said on the What Bitcoin Did podcast.

Trading of bitcoin vs. stablecoins and fiat currencies

Source: CryptoCompare

Building on other cryptocurrency networks

According to Tether, its digital tokens allow users to store, send and receive a currency that’s pegged to dollars, euros, and yen person-to-person, globally, instantly, and securely for a fraction of the cost of any alternative.

All transactions in tether, including the amount of tethers in issue, are recorded on the open-source bitcoin and ethereum networks (or ‘blockchains’).

This is because most tethers are issued on a platform called Omni, whose data is embedded into the bitcoin blockchain. A smaller volume of tethers in issue is linked to the ethereum blockchain, using ERC20, a technical standard that is native to that network.

Using established blockchains to record details of the tethers in issue offers advantages, say the token’s supporters.

“Since the original version of tether uses the bitcoin blockchain it inherits the inherent stability and security of the longest established blockchain network,” Tether says on its website.

According to a recent article in Bloomberg, tethers are now being issued on other blockchains too, including Liquid Network, Tron, EOS and Algorand. In May, the Block reported that tethers would be tradeable on Lightning, a second-layer payments network operating on top of bitcoin, by the end of the year.

Some of those blockchains are reportedly also working on adding privacy features that will disguise the nature of tether transactions. This could help broaden the cryptocurrency’s appeal for those seeking to evade capital controls, sanctions or the taxman.

Questions over asset backing

But it’s the fiat currency element of tether issuance that’s proved more controversial.

Tether says that tether units are created when a user deposits fiat currency into its bank account. Tether then credits the user’s account with the equivalent number of tethers, which then enter circulation.

But there has never been a full audit of the cash reserves backing the digital tokens. And earlier this year Tether watered down earlier claims that its tokens were backed one-to-one by dollars or other fiat currencies held at banks.

Prior to February 2019, Tether had said that its tokens were fully backed by traditional currency held in bank accounts.

However, in March 2019, Tether changed this disclosure, stating that henceforth tether tokens would be backed not only by currency reserves, but also by loans made by Tether to third parties.

“Bitfinex and Tether engaged in a series of conflicted corporate transactions”

In its ongoing lawsuit, the New York Attorney General said that the tethers in issue were now in fact partially backed by loans to an entity, Bitfinex, that’s not just a third party, but a related one.

The loan by Tether to Bitfinex, said the Attorney General, had been prompted by financial problems at the exchange in late 2018, when Bitfinex lost access to client funds held at third party payment processors.

“In order to fill the [funding] gap [at Bitfinex], executives of Bitfinex and Tether engaged in a series of conflicted corporate transactions whereby Bitfinex gave itself access to up to $900m of Tether’s cash reserves, which Tether for years repeatedly told investors fully backed the tether virtual currency ‘1-to-1’,” the Office of the Attorney General said in an April press release.

In early July Bitfinex issued a statement, saying that it had repaid $100m of its loan from Tether.

In his What Bitcoin Did interview, Phil Potter dismissed allegations that tether was unbacked, while admitting that the digital token’s asset backing had been watered down.

“The CFTC has been looking at tether since December 2017, allegedly. How long do you think it would take them to discover a massive fraud of the money not being there? But Tether has been able to print billions more since then,” said Potter.

“The reason the New York Attorney General is looking at this is the transaction that occurred between Bitfinex and Tether. This means that tether’s asset reserves only accounted for 74% of total assets. But this proved that tethers were fully backed dollar for dollar up until then,” Potter continued.

“Every stablecoin is fractionally reserved if you look upstream to the bank”

Tether’s defenders accuse critics of hypocrisy, particularly since fiat currency held in bank accounts carries its own risks.

Deposits with banks are not individually segregated for the benefit of each account holder, but instead are mixed with other client deposits and used to support new loan issuance by the bank. In total, this loan issuance usually far exceeds a bank’s deposit base.

And since the introduction of new, post-crisis regulations aimed at limiting the fallout from future bank insolvencies, anyone making a wholesale deposit at a bank is liable to face a ‘bail-in’ (a write-down of the deposit’s value and a forced conversion to equity) if a bank fails.

“Every stablecoin is fractionally reserved if you look upstream to the bank,” said Potter.

Others suggest that the move by Tether away from full reserve backing makes the cryptocurrency little different.

“The money is gone, and bitcoiners are rapidly learning to love fractional reserve banking,” Frances Coppola, a commentator on banking, wrote in Forbes in April.

“Tether is so important to the bitcoin ecosystem that they dare not reject it. Bitcoiners, like everyone else, are only too ready to abandon their principles to preserve their wealth. And so the cryptocurrency world becomes ever more like traditional finance,” Coppola said.

Tether’s utility and drawbacks

But these arguments may prove moot if users decide to adopt tether for other reasons.

Three key advantages of the digital token are its speed, accessibility and cost.

A tether transaction is considered final within sixty minutes, while a transfer of US dollars through the global banking system can take up to five business days.

And tethers turn over frequently, limiting the credit risks of those using the token. For example, according to CoinMarketCap, turnover in tether in the 24 hours ending 7am UTC on 7 August was $22.3bn, over five times the digital token’s market capitalisation.

“It’s got all the qualities of crypto—transferability and security—and it’s open 24/7”

While access to tethers is unrestricted, the US government controls access to the dollar payments system by means of a system of registration, monitoring for suspicious activity and heavy penalties for non-compliance.

And while international wire transfers in US dollars may cost $50-60 for a round trip, the principal cost of using tether is the bid-offer spread charged by intermediaries.

“It’s got all the qualities of crypto—transferability and security—and it’s also open 24/7,” said Phil Potter, tether’s co-founder.

One key disadvantage of tether is the variability of its market value, although this has died down in recent months.

Tether suffered significant discounts to its one-dollar target value in 2015, 2017 and late in 2018, and has also risen to an occasional premium to par.

Challenging the dollar standard

For global traders using the digital token to transfer value across borders, these periodic price fluctuations may be outweighed by tether’s utility.

“If you’re in Ukraine and you want to import cotton from Sudan, you don’t want to use each other’s bullshit currencies,” said tether’s co-founder, Phil Potter.

“You want to settle in hard currency like dollars. But that’s almost impossible to do now. US dollars are now very difficult to use outside the G7,” he said on the What Bitcoin Did podcast.

“This is a very big problem for the US dollar in general”

“Tether serves a very useful purpose: it’s a digital cash unit that people can push and reconcile quickly,” Charles Hayter, CEO of CryptoCompare, told New Money Review.

“The beauty of it is that it removes distance. You can pay money to anyone anywhere,” he said.

Stablecoins are seeing other uses in foreign markets, according to tether’s co-founder.

“In Asia, people are using tether as collateral when the US banks are closed,” Potter said.

According to Potter, the increasingly aggressive US rules on access to the dollar system could create a backlash and signal trouble for the monetary regime.

“This is a very big problem for the US dollar in general. And in the long term this will have a very chilling effect on the dollar as the world’s pre-eminent reserve currency,” he said on the What Bitcoin Did podcast.

This prediction may seem outlandish, coming from the creator of a token which has been plagued by controversy and whose daily turnover—$22bn—is dwarfed by the average $4.4trn that passes through the global foreign exchange market via the banking system.

But its worth remembering that the global financial markets have in the past proved quick to innovate in response to heavy-handed regulation.

In the 1950s and 1960s, the offshore eurodollar market grew up in response to attempts by US authorities to limit the interest payable on dollar deposits held by foreigners.

There was also, like now, a geopolitical angle: In 1957, the Soviet-owned Moscow Narodny Bank shifted its dollars from US banks and deposited them at its branch in London, helping support the new eurodollar business.

This time the controversy focuses not on interest payments, but on the US-led rules that control access to the banking system, and which are officially aimed at combating money laundering and terrorist financing.

If tether itself seems far too small to challenge the dollar standard directly, its invention and the continuing inability of the US authorities to stamp it out could be offering an early warning of a similar shift in global money politics.

Don’t miss any more New Money Review content: sign up here for our newsletter

Support New Money Review on Patreon or in cryptocurrency